| 作者 |

留言 |

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

Tycoon in the making

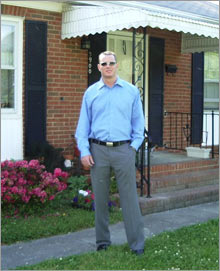

Still in college, real estate investor Saverio Fulciniti is a young man in a big hurry.

February 14, 2005: 10:16 AM

Saverio Fulciniti

Saverio Fulciniti

有些人从小胸怀大志,尽管还在上学,年轻的地产投资人Saverio Fulciniti已经开始挣大钱了。

NEW YORK - Some people are ambitious from a young age. They're early onset entrepreneurs who can't wait to start making money.

Take Saverio Fulciniti, 21. He came to the Boston area as a three-year-old from Calabria, the region forming the toe of the Italian boot. His mother was returning to America, where she had lived from age nine until after high school. Saverio's father was strictly Italian and spoke no English when he immigrated, at 28, to the States.

He was a trained electrician though, and soon obtained a license to practice the trade in the United States. Saverio's mother made her career in real estate, first in sales, then in property management.

"Both parents have had a big influence on me," says Saverio. "My mother is a tenacious business woman. I think her tolerance for risk and her business skills have made me the business person I am."

Like father . .... 有其父……

The immigrant work ethic rubbed off.

14岁开始在超市工作,16岁在Target,18岁每月挣$3,500 - $4,000,现在做DJ,并已几次买卖房产,从中净赚$69,500.

"I started working as soon as I could," Saverio says, "first in a supermarket when I was 14 and then in a Target at 16." He also toiled weekends and summers with his father and uncle as an electrician's apprentice. Even now, he acts as a private-function deejay and emcee.

During his freshman year at Northeastern University (from which he's scheduled to graduate in spring 2006) he started his own company called Level 5 Productions, which planned parties at local clubs and bars -- even cruise liners.

He says he made about $3,500 to $4,000 a month, but it was very stressful. He had other students working with him and they could be an undisciplined lot. "It's difficult trying to manage young college kids when you're just an 18-year-old yourself."

Saverio has a double major in Entrepreneurship and Marketing and lived on campus for two years. "I wanted to spend the first years on campus." But he knew he wanted his own home after that.

His mother helped by finding a place for him to buy ?a condo 30 minutes from campus in Danvers, Mass. ?and with a little financial help at closing.

Saverio himself met the bulk of the expenses, a considerable undertaking for a 19-year-old. The price was $130,000, not bad for 500 square-foot, one-bedroom with an open layout, but his mortgage lender looked at his age and minimal credit and wanted him to put nearly 30 percent down to avoid private mortgage insurance. He wound up spending $37,000, a sum he had managed to save from his many jobs.

That deal went through in July 2003. Since then, judging from sales of comparable apartments in his 45-unit complex, he says his apartment is worth about $160,000.

Irresistable impulse

He thought he was finished buying real estate until after graduation. Then his mother ran across a very undervalued apartment in a complex in nearby Amesbury in July 2004. He thought he was finished buying real estate until after graduation. Then his mother ran across a very undervalued apartment in a complex in nearby Amesbury in July 2004.

"It was being shown by an out-of-town broker who didn't know that comparable condos were selling much higher," says Saverio. He and a partner, Chris Limauro, "got an agreement to buy it in less than two weeks."

They picked up the one-bedroom place for $82,500, not underbidding by too much because they were anxious not to lose the deal. They put in some cosmetic repairs ?new hardware,painting, recessed lighting ?and had an offer on the place a week later. They sold it in less than a month and netted more than $20,000.

They turned around and bought another condo, this time a two-floor, two-bedroom townhouse, for $122,500. This one needed a little more work. They refinished foors, painted, put in new carpeting, and did electrical work. They also put on a new deck and windows. They sold it for $166,500 a month later.

With winter coming, Saverio and Limauro slowed down. But they are eying condos at two more complexes. "We're trying to put together a five-unit purchase for a spring closing," says Saverio.

Looking toward the future

展望未来

After he gets his degree, Saverio plans a career in commercial property finance. But his home town region is becoming a tough place to find investment properties. Building sales prices have outpaced rentals.

"Not many places in the Boston area can really generate cash flow," says Saverio.

In the meantime, he's in a co-op semester at school. Northeastern is a five-year program, in which students spend multiple semesters in the work force.

Right now, Saverio is working for a commercial mortgage broker, in addition to his property buying. He also will be going for his broker's license next month.

It may be tempting to think of Saverio as money conscious and frugal. But he is not a super saver by any stretch; he has very normal spending patterns for a college student.

There may be something in the name, though. Saverio is Italian for Xavier, a Spanish name that means ?"New House."[/size]

毕业后,打算从事商业地产金融。目前正在为商业地产经纪人执照而努力。他的名子在西语的意思是“新房子”。

|

|

|

|

最后进行编辑的是 LOOKING on 2006-02-23, 14:41, 总计第 3 次编辑

|

|

|

|

|

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

Tycoon in the making

For the young immigrant Tamara Garber, real estate opens the golden door.

房地产为年轻的移民Tamara Garber 铺设了一条金光大道

Tamara Garber

Tamara Garber

同老一代移民一样,来到美国,没有钱财,有的只是聪明、勇气和成功的欲望。

NEW YORK - Like generations of immigrants before her, Tamara Garber arrived in the United States with little more than intelligence, courage, and desire to succeed

Garber 在前苏联的乌兹别克斯坦长大,但却找不到希望,就来到了美国。Garber grew up in the ancient silk-route city of Tashkent in Uzbekistan, the former Soviet republic. After the breakup of the Soviet Union, the central Asian country became increasingly inhospitable to non-Uzbekis. As someone of Russian-Jewish ethnicity, educational and career advancement there seemed unlikely for Garber.

So in 1994, she, her mother, and her brother came to New York, where her older brother was studying medicine.

Immigration was wrenching. "It was most difficult to know and realize that there's no life here yet and there's nothing to go back to," she says.

At first, her version of the American Dream seemed more like a nightmare: Up every weekday at 4:30 so she could open a coffee/bagel shop, premed classes in the afternoon at NYU, home rarely before 10:00, and weekends filled with baby-sitting jobs. She had to earn a living and help support her mother and brother.

"When you're an immigrant you have no one to rely on," she says. "You have to make your own way."

After she realized that a career in traditional medicine was not for her, she switched to acupuncture, which she still practices.

First blood

Garber was working in a computer store and going to school full time when, in 1999, she bought a co-op apartment in the Bronx for her mother. Her first venture into real estate was not an altogether happy experience.

She was 22, with no credit history, and little money. Mortgage loan officers gave her the runaround. Four co-op boards turned her down. Finally, she found a sponsor's unit in a building in Riverdale that didn't need board approval.

Garber paid down $8,000 and took on a $32,000 mortgage, which "seemed huge," she says. Her mother stayed for a couple of years. Tamara then sold the apartment for a profit of about $25,000.

She began to study motivation -- the desire to succeed and taking action to make it on your own. She also got into her next real estate venture, buying a three-story, single-family house in Englewood, New Jersey at a foreclosure sale for $125,000, a week after the World Trade Center catastrophe.

"I had no idea what I was doing," she says. "I didn't see the house prior to bidding, I didn't know basic things such as needing to check the title history for liens." She found that she had bought a wreck -- with the previous owner still on premises.

She had neither the time nor the money for legal bills to force the old owner out. Tamara weighed her options and made her an offer. "I paid her to move out," she says. "At $3,000, it was cheaper."

The house was structurally sound, but filthy. ("It had cans of food from the 1950s in the kitchen," says Garber.) After six months of work -- a new roof, siding, drywall, floor, kitchen and baths, and fresh paint -- the house sold for $259,000, a profit of about $70,000.

Knowledge is power

知识就是力量

Her next purchase was a single-family unit in Englewood Cliffs that she wanted to tear down and rebuild. Over the next year she experienced the pain of navigating a maze of variance approvals, public hearings, and publishing notices in local newspapers. She bailed out more than a year later without starting the project, but she received $80,000 more for the property than what she paid.

She began to make it her business to learn more about the business. She read books and magazines, listened to motivational CDs, and talked with others in the business. Eventually, she even took a job with a mortgage lender.

"I learned everything I needed to know about financing," she says. "Now, when talking with bankers, I know exactly what they're saying."

Garber started to think about getting into home construction. She bought an old house in Edgewater, razed it, and built a duplex, the biggest house in town. She needed to bring in a partner to accomplish this, and the deal yielded more than $400,000 in profits.

Since then she has begun constructing three more two-family houses in Edgewater. Her latest step is buying a five-lot property, where she will build three duplexes and two single-family homes.

Garber has certainly benefitted from the rapid expansion of real estate prices. She insulates herself from short-term downturns by selling quickly.

Determination and an ability to act characterize her temperament. "My banker told me that other people say why this deal or that deal won't work," Garber notes. "She said, 'But you, you just go out and make it work.'"

Garber still feels like a rookie. She wants to learn more and recently enrolled in her first real estate course, a seminar at NYU conducted by leading developer. She's looking for her next project.

"I love the challenge of real estate," says Garber. "I take so much pride when I pass a house I built, knowing that families are living there."

|

|

|

|

最后进行编辑的是 LOOKING on 2006-02-23, 14:40, 总计第 1 次编辑

|

|

| |

|

|

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

They call them flippers

Buy. Sell. Profit. Repeat. Investors are flipping houses to build wealth. Here's what you can learn.

NEW YORK - In the 1990s, Flippers were stock jockeys who finagled their way into initial public offerings, only to flip them days or hours later for big profits.

These days the go-go market is homes, not stocks. In hot spots like Las Vegas and Florida, real estate flippers have discovered that a modest down payment and a little patience can net them tens (even hundreds) of thousands of dollars in profits, sometimes tax-free.

The most aggressive of them figure that some combo of paint, new flooring and kitchen upgrades can turn the dumpy house they bought for $300,000 in February into a $400,000 property they can unload in July. And in the most sizzling markets, they're absolutely right.

Ask Angel Cooley, 54, a retired judge who moved to Las Vegas three years ago and has since flipped eight houses. Even with the Vegas market cooling somewhat in recent months, Cooley expects her real-estate-related net worth to reach seven figures this year.

"A year ago you could buy something in Vegas for $200,000, and in less than four months you could gain $150,000," she marvels. "It was a crazy kind of hysteria here, like people running after a Brink's truck."

Sound tempting? Absolutely. While quick-hit real estate investing is nothing new, the confluence of new tax breaks, low interest rates and exploding prices has created a perfect storm for flipping opportunities (at least in some markets) and has made legions of instant moguls.

Problem is, the playing field is getting crowded. In Las Vegas, 7 percent of all homes sold last year had been owned for less than six months, according to DataQuick Information Systems. Nationally, 14 percent of all new mortgages these days are for second homes or investment properties, up from 8 percent in 1999, reports mortgage tracker Loan Performance.

If you've been considering putting in your application for that real estate mogul position, statistics like these should give you pause. So should the example of veteran flippers like Jeff Bliven, who, after 20-plus years in the game, says he's dropping out.

"With some of these mortgage companies, if you can fog in a mirror they'll make you a loan," says the 42-year-old resident of Newtown, Conn. "When everyone's doing it, it's time to liquidate."

Some facts to keep in mind.

Speculation makes markets riskier. That's what concerns David Berson, the chief economist at Fannie Mae. He's still bullish on home prices but worries that speculators may overinflate white-hot markets.

Historically, home prices have declined very infrequently in the U.S., in part because typical homeowners don't treat their houses like stock investments. They don't sell in a panic just because their neighbor fetched only 90 percent of his asking price.

"But the nature of speculators," Berson notes, "is that they do pull out when prices stop going up."

Even a small downturn could wipe you out. Vegas or Miami or San Diego real estate surely won't lose all of its value like an eToys, but the potential risks for investors are just as dire.

A flipper who puts down $40,000 to buy a $400,000 home would lose the entire down payment should the market decline just 10 percent; throw in closing costs, 12 months of mortgage payments and a 6 percent realtor commission to sell, and the flipper could easily be out $80,000 on a $40,000 investment.

Hard-core flipping is obviously not for everyone. If the market chills, you'll face the ignominy of making monthly mortgage payments on a property you can only sell at a loss. That said, the risks are mitigated when you live in your investment for at least two years. Not only are the potential tax benefits terrific, but your mortgage payments cover an all-important cost of living: shelter.

So what's the best way to get started? MONEY sounded out two dozen experienced renovators and real estate investors around the country for suggestions. Here are the highlights.

Lesson 1: There's a reason it's called sweat equity.

Flippers who do put down roots -- perhaps they're more aptly described as serial renovators than as flippers -- typically buy unattractive or underappreciated houses in good or up-and-coming areas. They live there while making key renovations and then sell after two years, all the while looking for their next two-year home improvement project.

Why wait two years? Under current tax law, the first $250,000 of profit from a home sale is tax-free if the seller has lived in the house for at least two years. The tax break is even bigger for married couples: The first $500,000 in capital gains is tax-exempt.

"For the typical American, it's the best and most generous tax break in the entire tax code," says Douglas Duncan, chief economist for the Mortgage Bankers Association.

Turning a profit may seem easy in a flippers' market, but getting from point A to point B can be a lot of work, particularly if the brand of investing you're used to is of the point-and-click variety. Scouting out properties, negotiating financing and final prices, and overseeing renovations can be a full-time job.

In fact, real estate is as much a lifestyle choice as it is an investment strategy.

Serial renovators Bob and Christine Miller of Phoenix, for instance, spend most of their free time working on their homes, doing everything from repainting walls to rummaging through junkyards for vintage doors and sinks. For 44-year-old Chris, home improvement is in the blood: Her dad was a weekend tool-belt warrior. But Bob, a 41-year-old baseball executive with the Arizona Diamondbacks, didn't know Bob Vila from Bob Uecker before he met Chris.

Soon enough, though, he was tiling floors and installing cabinets like a pro. He says that fixing up a neighborhood eyesore is almost as rewarding as turning a big profit. "You have to enjoy doing the work. And we do."

Lesson 2: You can't sell high if you don't buy low.

Even a world-class do-it-yourselfer with a keen eye for design can't turn a bad house in a bad school district (or a good house purchased for too much) into a winning flip. That's why most flippers focus their searches on ugly ducklings that can be turned into swans with a few cosmetic changes.

"I look for the house that the neighbors hate because it's not kept up," says Joyce Grimes Bone, 37, of Norcross, Ga., who has flipped 10 homes in four years.

Her rehabs typically cost about $10,000 per house and are what she calls "cosmetic light," meaning carpets, roofs, paint and landscaping. The goal is to make $20,000 in profit per deal. For the math to work, she must buy 30 to 40 percent below a home's post-rehab market value.

Bone takes a Peter Lynch-ian, buy-what-you-know approach. "My niche is suburbia," she explains. "If it's on the way to Costco, I've checked it out."

Before bidding, she runs through a mental checklist: "Do the neighbors have pride of ownership? Are the schools good? How close is it to shopping and the highway?" It all boils down to whether she'd want to live there.

The thing is, not every neighborhood has a "Boo" Radley house in dire need of a makeover. And if you're looking for bargains, real estate agents aren't likely to be much help because their job is to get top dollar for sellers, not steals for buyers.

Bone, like many flippers, looks to the foreclosure and pre-foreclosure market to find motivated sellers willing to cut a deal. Locating these folks isn't easy (Bone goes so far as to post "We Buy Houses" fliers at the county courthouse), but the Internet does help.

Check out foreclosure and pre-foreclosure Web sites such as RealtyTrac.com for leads to investors looking for off-price real estate.

Lesson 3 Practice makes perfect.

Celestino Mastrangelo, 42, of Willoughby Hills, Ohio, has been investing in real estate for a decade. His first deal was a clunker. After making only cosmetic repairs, he and brother-in-law Dino Scalzo put the house back on the market, only to have it go unsold for months. The problem? Dingy kitchen cabinets and a prehistoric furnace turned off buyers.

"With our second house," he says, "we did everything: new kitchen cabinets, new furnace, hot-water tank, and we finished the basement." After putting $25,000 into the $80,000 house, they soon sold it for $155,000. "You have to spend money to make money," he says.

Mastrangelo also learned to line up financing early. If you're selling one house to buy another, you'll probably need a bridge loan. For hard-core flippers hunting for quick scores, traditional mortgages may not do the trick.

The best bargains come from people who need cash and are in a hurry to sell. That's why many flippers finance purchases either with personal savings or home-equity loans.

Says Mastrangelo, "Sellers are motivated to sell to you when you don't have to qualify for a loan."

Lesson 4: You don't need to flip to add value.

The tricks of wise flippers can be applied to your home, even if you've no plans to sell. When they buy, they look for places that are underpriced because of cosmetic problems that most house hunters don't realize can be easily fixed.

When they renovate, they choose styles, patterns and fixtures with broad appeal: no purple kitchens, no heart-shaped Jacuzzis. Installing an ultra-efficient furnace or carving out an attic bedroom is nice but unlikely to enhance a home's curb appeal.

That's why the most fruitful fixes are the most visible ones: floors, siding replacement (in colder climes), outdoor decks (in warmer regions), bathrooms and all things kitchen -- cabinets, counters and appliances.

And when it comes time to sell, the first thing they do is paint. "Exterior, interior walls, trim, ceilings, everything," says Bone. "The greatest payback is things people see."

|

|

|

|

最后进行编辑的是 LOOKING on 2006-02-23, 14:38, 总计第 1 次编辑

|

|

| |

|

|

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

Sharing cash, contacts and contractors

Kiyosaki fans stop playing the board game and partner in real-world real estate ventures.

NYC Cashflow founder Ed Patisso gives the ins and outs of home finance to a group of newcomers.

Former Buffalo resident Lewis Hudnell points out up and coming zip codes to a group of potential investors. Former Buffalo resident Lewis Hudnell points out up and coming zip codes to a group of potential investors.

NEW YORK - On a recent night in midtown Manhattan, a group of people gathered for an exercise in real estate networking that would make any self-help financial guru proud.

Some members of the diverse group knew each other from past meetings where they would play Cashflow, the board game based on the teachings of "Rich Dad, Poor Dad" author Robert Kiyosaki.

But they were through with game playing. That night they were there to pick up the name of a good contractor, the number of a trusted real estate lawyer, or to offer cash, credit or time as one member of a real estate partnership.

In short, they were ready to turn a game about getting rich into a game plan for getting rich.

"It's happening, people are networking and they're sharing resources and they're buying real estate," Ed Patisso, who founded the group, known as NYC Cashflow, told curious members at the start of the meeting. "If you don't have a couple hundred grand in the bank but have a few dollars and want to invest, you can do it."

The deals

Real estate is the most popular investment choice, largely because it's so favored by Kiyosaki. And Buffalo or Philadelphia are the preferred markets, partially owing to New York City's prohibitively high prices.

New York City resident Joseph Patton, 34, met Patisso through NYC Cashflow in the fall of 2003. Soon after they invested $54,000 cash for a rental property in Buffalo; $19,000 to buy, $30,000 to fix up and another five grand in other costs.

Patton says the property is now worth $85,000 and the two pull in $600 a month in rent, after all expenses. Plus they took out a home equity loan on the house to repay their initial investment and free up the cash for other purchases. They have since bought two more similar properties.

Patton says he's learned enough in these first deals to branch out from partnering with Patisso and will look for other people in the Buffalo area, where he plans three more buys. He also says he thinks he's ready to start acting as a mentor himself.

"The group led me from four or five years studying it, thinking about it, to finally taking action," Patton said. "It's worked phenomenally for me."

New York resident, 49, Percy Keeley bought a three-bedroom, one-family house in Buffalo at foreclosure for $11,000. He then spent $22,000 on renovations.

Percy says he now rents out the house, with a property management company taking care of all the details. After all his expenses, including the mortgage, management fees and taxes, he says he sees $250 in income every month.

"I ended up relying on a lot of people in the club to help me do this," said Percy, who listed lawyer, banker and real estate broker referrals as well as general support as things he received from the group.

Risks

Is partnering up with near strangers for such large investments just inviting trouble?

Steve Greene, who is active in the group and also acts as its spokesman, said NYC Cashflow is always on guard for fraudsters and recently had to remove a posting from its Web site that was trying to lure members into forming a partnership and buying a property. It turned out the person who posted the ad also owned the house for sale.

The group is also trying to develop a rating system on its Web site that will let members rate each other in terms of honesty or work ethic, patterned after eBay's method of rating sellers. But Greene says the biggest thing keeping people honest is their regular meetings and the bonds that have developed.

"When you're meeting time and again with 40, 60, 80 people in the same room," said Greene, "word gets around."

There's another problem. If buying property on one's own can be full of hassles, partnering with one or two relative strangers could turn into a logistics nightmare.

Patton says to keep things simple, he and Patisso have divided up the basic chores of running a rental property. Patton does the bookkeeping and pays the bills while Patisso deals with the contractors and property management company. And they pass files back and forth electronically.

"Once the properties are up and running, there is very little maintenance that requires a face-to-face meeting," said Patton. "But we have the same files at all times. As joint owners, you need to have that."

They also have a written contract between the two of them that says if one partner wants out, the other partner either needs to buy out his half at "fair market value" or put the property up for sale.

Interested in attending a meeting? Greene said there is no clause requiring a commitment to join any deals or buy anything. He said that the only cost to attend is the fee for the space, which Greene said is less than $5 when split between everyone.

He also said there has been so much interest from newcomers to real estate that the group is thinking about starting a $160, 16-hour real estate class for beginners.

And a spokeswoman for Robert Kiyosaki said the New York group isn't the only one that has branched out from the board game, although it was hard to tell exactly how many of the 800 loosely-organized Cashflow clubs worldwide were planning real-life deals.

|

|

|

|

最后进行编辑的是 LOOKING on 2006-02-23, 14:34, 总计第 3 次编辑

|

|

| |

|

|

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

Tycoon in the making

When the Internet bubble burst, Dave Goldoff left the industry and headed out into real estate.

NEW YORK - Dave Goldoff once shunned the real estate business, despite the success his father and uncle had with a few buildings they bought together in lower Manhattan. NEW YORK - Dave Goldoff once shunned the real estate business, despite the success his father and uncle had with a few buildings they bought together in lower Manhattan.

For Dave, real estate seemed too conventional.

Instead, he worked in Internet entertainment, a fast-paced world where he rode a roller coaster of different jobs. Projects ended with mass layoffs or a neat corporate crash-and-burn.

When the bubble burst, he found himself idle and living in a family apartment building on Water Street in Manhattan. His uncle suggested he earn back some rent by running the building.

"I liked it because I could see things happening," he says.

"In 2000, they were getting $1,800 a month for a one-bedroom apartment," he recalls. "I spent $20,000 to $30,000 to renovate and the rent went up to $2,300."

Then came September 11.

The building lies eight blocks downwind of ground zero. Goldoff had been at the Twin Towers that morning. Back home, he heard the first plane crash. "I thought the cooling tower on our roof had fallen." He was outside when the second plane hit.

Everyone evacuated, but authorities called Goldoff back in because they wanted to use the roof for communications devices.

"I saw a warship in the river, fighter planes patrolling overhead, and armed guards around the building, which was covered with soot," he says. The stench from the burning buildings lasted for weeks.

"A lot of tenants were stressed out and walked away from their leases," he says. "But we couldn't go after them for leaving."

Getting started

Managing the building piqued Goldoff's real estate instincts. He decided to go back to school at night for a degree in the field. He's now nearing the end of a four-year course of study at NYU.

Early on, he took a job with a real estate investment firm. "My uncle told me to learn how people buy and sell properties," he says. "What I learned was that I didn't want to be a broker."

He started going around the city, trying to get a handle on prices. He looked at many dilapidated buildings with an eye toward buying them cheap, doing a quick fix-up, and selling fast.

"I met people doing foreclosure flips," he says. "I went to auctions, and I sat and listened. I had no money and no clients."

He decided the best, low-risk proposition would be to buy land. He and a high school friend, Erik Orsino, partnered up to start a company, D&E Management.

They bought their first property in June 2003, a commercial-zoned lot in Far Rockaway, paying $80,000 at a foreclosure auction for it, putting down 10 percent. They planned to sell the contract within 30 days -- to avoid closing costs -- to a client who was willing to pay $125,000.

It sounded great: Put down $8,000 and get back $45,000 less than a month later. But title problems plague foreclosures.

"I would guess that 99 percent of auctioned properties don't have a clear title," says Goldoff. Either an old owner is still on the deed or there's a tax lien or the land has wetland issues.

The lack of a clear title is not always a disadvantage. According to Goldoff, it can buy time. Ordinarily, you must complete the deal within 30 days, which means coming up with the balance of the money.

"Auctioneers are responsible to make sure the title is clear," he says. "If it's not you can delay the closing or get your deposit back."

In the end, that "quickie" first deal took a year. But they came out of it with a $20,000 profit and a learning experience. They completed three more deals like that, before the auction game grew too crowded to continue.

"There was no room to make money," says Goldoff. "We pulled out. We had to figure out a new vehicle."

Greener fields

They turned to upstate New York. The first house they bought there was a three-bedroom, one-bath summer home on a lake in Orange County. They paid $225,000, spent $70,000 winterizing and modernizing it and putting in a second bath. It's on the market now for $450,000.

They've closed on three houses upstate, and are in contract to acquire an estate on the water in Bridgeport, Conn., where they hope to build several townhouses. Then there's an old brewery in Watkins Glen, N.Y., which they intend to buy and develop into a condo complex and resort.

"I target lakes and golf courses," says Goldoff, "places with better schools and good access to transportation."

The now 29-year-old Goldoff, who recently married Beth, a creative director he met in art school, strives to make money with each purchase. He doesn't count on a hot market to bail him out.

"I always have to look at the worst case scenario," he says. If the deal is profitable under those conditions, "Everything else is gravy."

Eventually Goldoff hopes to be in all three categories of real estate ?management, development, and sales, a "turn-key operation," as he calls it.

"Two years ago I was out looking to network," he says. "Today, people are calling me."

|

|

|

|

最后进行编辑的是 LOOKING on 2006-02-23, 14:33, 总计第 1 次编辑

|

|

| |

|

|

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

Tycoon in the making

Ted Theodoropoulos learned early how lucrative real estate investing can be.

NEW YORK - When Ted Theodoropoulos was about 10 years old, he learned a valuable lesson. NEW YORK - When Ted Theodoropoulos was about 10 years old, he learned a valuable lesson.

"My father bought a corner house in Chapel Hill for $60,000," says Ted. "He intended to knock it down and build another. But before he had a chance to do that, they announced that a mall was going in directly across the street."

His father wound up selling the property six months later for a cool $200,000 profit.

"It was mostly luck," says Ted. "But it made a big impression on me."

Perhaps it has helped focus Ted's entrepreneurial attitude. The 32-year-old North Carolinian has invested in three properties during the last two years and is looking for more.

Ambition and Ted are well acquainted. His mom and his dad have both been business owners, in addition to dabbling in real estate. Ted himself started a company, a collection agency, when he was still in college.

It was his mother who made the suggestion that launched his company. She was a restaurant owner who had taken some bad checks and she didn't have the time to pursue them herself. She told Ted she would give him a fee for any accounts he was able to make good.

Ted was so successful that he dropped out of school and started a collection agency. It began with restaurant clients, then branched out to corporations, such as Lucor and Time Warner Cable, for which he collected equipment when customers moved away or fell behind in bills.

At the peak, Ted employed 15 to 20 people. He ran it full time for a year as he attended night classes. It proved lucrative enough that his mother and a brother joined the business.

After college, where he studied information technology, Microsoft offered him a good job, "50 percent more than I was making at the collection agency," he says. So he turned the collection business over to his brother and mother, and went to work at Microsoft's Charlotte office.

He stayed there for a year or so and then went to work crunching data for a major bank, where he is a vice president today.

First foray

In 2001, Ted made his first real estate purchase, a one-bedroom condo in downtown Charlotte. He he paid $145,000 and it's now worth about $235,000.

Watching the value soar "got my wheels turning." At the time, a bank colleague was supplementing her income flipping properties regularly. "She was not hitting the ball out of the park," he says, "But she was doing well."

Through her, he met a broker who asked about Ted's means and goals: How much did he have to invest? Did he want to manage the property? What return was he looking for, and in what time frame?

"He gave me a realistic picture of the business," says Ted. "A lot of it -- like cleaning up after tenants and chasing them for rent -- is undesirable."

But Ted was used to working with credit reports and "skip traces," which enable collectors to track down people. So in early 2002, he bought a three-bedroom, one-bath, brick ranch near a gentrifying part of town. He paid only $72,000 plus a little more fixing the cosmetics and installing new air and floors.

"I rented it out for a year," he said. "Then my mother and brother moved down to Charlotte and started living in the place." The two had put up some of the money for the house, as they have with subsequent ventures. The home's value has risen to the low $90s.

Shopping for foreclosures

The next step was to plunge into the foreclosure market. This is always a gamble because home inspections can be difficult to arrange making it tough to analyze how much more cash will have to be invested. On the other hand, foreclosures can be great bargains.

Ted, for example paid less than $40,000 for two condos near downtown Charlotte. The first, a one-bedroom, was just $17,000. He rents it for $500 a month and values the property at $35,000 today.

The second is a two-bedroom, one-bath, 900-square-foot he closed on last December. One of the reasons it interested him is that the condo board was spending to improve the property.

"There's an undesirable neighborhood next to the condos and it's keeping the property values down," says Ted. "But the board was talking of a special assessment to pay for a fence to block it off from the bad area."

He felt that with such steps the apartment would be worth much more than the $22,000 he paid. Ted wants to sell this apartment and has put it on the market for $44,500, which would mean a profit of $20,000.

Although he has proceeded cautiously, Ted envisions expanding more rapidly. Right now, he wants to do more low-risk deals until he learns the real estate business inside and out.

Ultimately, he would like to involve his two other brothers in it as well.

"When you're working with your brother, you know you're going to get a straight deal," he says.

|

|

|

|

最后进行编辑的是 LOOKING on 2006-02-23, 14:29, 总计第 1 次编辑

|

|

| |

|

|

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

Tycoon in the making

Cody Kennedy has morphed from fiscal conservative to risk taker.

Toronto - Growing up along the Front Range of eastern Colorado, Cody Kennedy got a good grounding in traditional ways: Respect your elders, eat your vegetables -- and always pay off your old purchases before you buy anything new. Toronto - Growing up along the Front Range of eastern Colorado, Cody Kennedy got a good grounding in traditional ways: Respect your elders, eat your vegetables -- and always pay off your old purchases before you buy anything new.

His family of ranchers and cattle owners, "is, fiscally, very conservative," says the 31-year-old.

So when he and wife Summer bought their first house in 1999, he didn't expect it to be the start of a real estate business. He had bought the family home, nothing more.

True to form, Kennedy put down a substantial payment (more than half) of the $143,000 he paid for the three bedroom, two bath house in Fort Collins.

Most of it was a gift from the family feedlot business. The rest came from savings from Kennedy's own insurance and financial brokerage business.

His business produces "erratic earnings," he says, some months bringing in five figures and others, zilch. "Whenever I got a big check I would pay off some principal."

The late 1990s and early 2000s were good years, both personally (the couple had two baby girls, Kathryn, now 4, and Elizabeth, 2) and professionally.

So he was able to pay off the mortgage in three years.

The transition begins

In the meantime, though, the real estate business began to interest him. He read books on the subject, including "Rich Dad's Real Estate Riches," and picked up different methods of financing home purchases.

In March 2002, he bought a bigger house in Fort Collins -- paying $243,000 -- to live in, and rented out the first. After a year and a half, he sold the first one for about $31,000 in profits and plowed that into the new place.

Then, he visited his local Wells Fargo banker and told her, "I want to use my equity to purchase other properties." The broker set him up with a line of credit amounting to 100 percent of the value he had in his house.

The line of credit enabled Kennedy to act quickly when he found a bargain, and it carried a low interest-only rate of prime plus 0.15 percent. Wells Fargo only requires a payment of $500 if he closes the line of credit within three years.

The cash came in handy in October of 2003 when the Kennedys moved across the state to Summer's hometown of Grand Junction. They paid $183,000 cash for a four-bedroom house there, and rented out the Fort Collins home for $1,075 a month.

Shooting for more

Cody then shifted into high gear. His brokerage business had slowed and he spent many weekend hours driving around looking at properties.

Last February, he found a nice brick single family in Centennial, Colo., near Denver, that he bought for $130,000. He did about $15,000 worth of work on it and had it reappraised for $230,000, which increased his line of credit to $207,000. He rented it for $1,095 a month. Last February, he found a nice brick single family in Centennial, Colo., near Denver, that he bought for $130,000. He did about $15,000 worth of work on it and had it reappraised for $230,000, which increased his line of credit to $207,000. He rented it for $1,095 a month.

In August, he bought a duplex, two side-by-side apartments in one building, for $137,000. One side was already rented for $575, and he had a tenant in the second, at $595, by the first of October.

[The Kennedys lived in Grand Junction by then. Across the street, a house similar to theirs had fallen into disrepair. The owner had lost his job and the family had moved out. As the home slipped toward foreclosure, no one would pay its asking price of $180,000.

The house sat so long that Cody made a deal for it for just $133,000. He put another $12,000 into the fix-up and now rents it for $975 a month.

That brought the total number of properties the couple currently owns to five, including the family home. Rents produce more than $51,000 and payments to the bank offset that by only about $25,000. Even with taxes and maintenance, he still makes a profit.

Bubble trouble?

Does he worry that he's stretched too thin?

No, for two main reasons. "All my properties cash flow pretty well," he says. "Even if interest rates go up another point this year, I'll still have profits."

Kennedy says he rents at slightly below market in order to have his pick of tenants, requires credit reports from applicants, and keeps the properties in excellent condition.

"My costs are low," he says. "I could carry all my rentals for a year and it wouldn't kill me." He says he will only buy a property that he judges a great value.

The markets these properties are in have not gone through severe price inflation. At last report, for example, Denver single-family home prices had risen at an annual rate of under 3 percent, and the average home sold for $250,000, considerably less than the sizzling hot markets in the Northeast and California.

So Cody is confident he can ride out any real estate storms and he's actively seeking more deals, and taking calculated risks.

It's all part of his transition from his conservative roots to wheeler-dealer.

|

|

|

|

|

|

| |

|

|

blogGreen88

游客

|

|

| |

|

|

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

Tycoon in the making

Jaz Wray is always on the move, picking up bits of property along the way.

Glendale, Az - Although still a comparative youngster at 32 years old, Jaz Wray has already lived in dozens of homes around the country and even internationally, from New Jersey to Brazil. Glendale, Az - Although still a comparative youngster at 32 years old, Jaz Wray has already lived in dozens of homes around the country and even internationally, from New Jersey to Brazil.

When Wray was growing up, his army dad father moved the family around a bit, but as an adult, Wray has really been in perpetual motion.

"Since 1988, the longest I have lived in one place was just over a year," said Wray. "In the past 10 years I've been in 15 different cities." Portland Oregon, Jonesborough Tennessee, San Francisco, and Rio de Janeiro, to name a few.

Along his peripatetic way, he's managed to buy a couple of the houses he lived in and he has held onto them even after he moved on. These purchases now form the basis of his burgeoning real estate empire.

The start

He was in his second year of college and selling LA Times subscriptions door-to-door when it came to him that he was building up too much debt. He didn't like that, so he dropped out of school and took a full-time job.

Wray has worked mostly in the telecom and contracting industries, serving on various projects over the years. The jobs often called for relocation.

A major benefit to this gypsy existence was that compensation sometimes included both a salary and per diem payments. "My expenses were paid and I was able to save most of my salary," Wray said.

That sometimes helped him afford to buy the house he lived in. In 1997 he was stationed in Dallas, where, he said, "Rents were high and home prices very low. It was a great opportunity to buy rather than rent."

He purchased a three-bedroom, two-bath house 20 miles west of downtown for $86,000. Then, when he moved several months later, he rented out the house. "It's cash-flow positive," he said, the rent more than paying off the taxes, maintenance, and other expenses.

The one thing the Dallas house has not provided is any extraordinary price gain. "If I had bought just about anywhere else, the house would have at least doubled in value," said Wray. But in Dallas, the house is currently worth only about $110,000, a modest 28 percent increase over eight years.

In contrast, his second purchase, in Buena Park, California, near Los Angeles, which he bought in April 2003, has already gone up more than that. He purchased the 1,000 square foot, three-bedroom, one-bath for $300,000 and he believes that it's worth perhaps $460,000 today, about 50 percent higher.

He has not turned a profit on the rents since he moved out last October, but he's building equity because the rent covers the mortgage.

Abandoned equities

Wray's house investments make up the bulk of his net worth. Like many 1990s investors, in particular those who worked in the tech and telecom industries, he lost quite a bit in the Nasdaq meltdown. That spurred him to re-evaluate his investing. Wray's house investments make up the bulk of his net worth. Like many 1990s investors, in particular those who worked in the tech and telecom industries, he lost quite a bit in the Nasdaq meltdown. That spurred him to re-evaluate his investing.

"I stopped putting new money in the stock market after that and began saving toward new real estate investing or paying down my home mortgage," he said. His investable assets, including savings and retirement accounts, amount to about $200,000.

His more conservative investing style goes hand-in-hand with his recent new responsibilities. In 2002 he married Shelly, and the couple now have two children, Jag, a-year-and-a-half-old boy, and Brazil, a brand-new daughter born this August.

The family moved to Glendale, Arizona, outside of Phoenix, last year and they bought their third property, a good-size (four-bedroom, two-bath) house. They paid just $155,000 for it. The Phoenix market has been among the hottest in the country lately -- through June 30 the 12-month gain there averaged 47 percent for single-family homes.

That means Wray has already logged a substantial paper profit on the new house. He estimates it's worth $250,000 today.

Strictly investment

With his father-in-law and brother-in-law, Wray went in as a partner this year on the purchase of a Phoenix area condo.

"We put a bit more than $40,000 into it," he said, "plus blood, sweat, and tears." The three replaced the floors, renovated the baths with new fixtures and tile, put new cabinet doors in the kitchen, and spackled and painted.

Even counting all that sweat equity, the condo seems like a bargain. It's strictly an investment that Wray hopes will appreciate with the Phoenix real estate market and become a cash-flow positive rental later this year. Meanwhile, his brother-in-law lives there. All told Wray has only put about $4,000 in cash into the property and figures that his share of profits, if sold today, would come to about $5,000.

The Wrays own the Dallas home outright, owe about $235,000 on the California property, and about $115,000 on the Phoenix house. That means they've accumulated approximately $475,000 in home equity on the four properties.

He said, "I plan to buy my next house as a primary residence again if the real estate market is good for the area (wherever that may be) and then try to keep the house as a rental if I can make it work."

Meanwhile, Wray has gone back to school in addition to full-time work. He attends Thunderbird Business School in Phoenix and is working toward an MBA in international business to "further my value to the workplace."

He has already done quite a bit to further his value in real estate.

|

|

|

|

|

|

| |

|

|

cialis generic viagra

游客

|

|

| In Oklahoma violators can be fined, arrested or jailed for making ugly faces at a dog. cialis generic viagra

|

|

|

|

|

|

| |

|

|

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

Tycoon in the making

Mary Buenavenura didn't start out to make a million on real estate -- it just worked out that way.

NEW YORK - Call her "The Accidental Tycoon." When Philippine-born Mary Buenaventura first started buying second homes, she didn't intend to become a real estate millionaire -- it just worked out that way.

"My prime goal in the beginning was simply to have a nice vacation home," she says. Maybe so, but now she owns three single-family homes and two condos, and has equity is the seven-figure range.

Andrea, Mary and Charles Buenaventura

When Buenaventura came to the United States in August, 1984, she brought excellent English skills and quickly got work as a clerk. That lasted a couple of months until she found a job as a legal secretary. She's worked in that field ever since.

She bought her first home in 1987, a town-house condo in Norwalk, Calif. But that was the year she had her first child, son Charles, and as a single mother, Buenaventura says she wanted a real house.

"I sold the condo after less than a year," she says.

This was during the late 1980s housing frenzy, and the condo had appreciated 50 percent, to $120,000, during the short period she owned it.

She applied the sale profits to a three-bedroom, two-bath nearby, where her family -- daughter Andrea arrived a few years later -- lived for 12 years. When she sold it in 2000, the price had appreciated much more modestly than the condo had, just $45,000 more than she paid.

Catching the wave

By 2000, when Buenaventura moved her family into their current home in La Habra, in Orange County, real estate was flying again. She got in under the high-wire, paying just $237,000. The home value has increased to $750,000.

Her first non-primary home purchase was a one-bedroom cabin near Big Bear, in the mountains out past San Bernardino. She bought it for family vacations in June 2001 and she paid $63,000.

The family only used it for a year or so before her children rebelled.

"You know how kids are," she says. "When they're younger, you can just tell them to pack up. But when they got older they wanted to stay home, close to their computers and their friends." Before that happened she had bought another cabin, intending to rent it out, not far away, for $75,000.

In 2002 she refinanced the La Habra house and her bank offered her enough extra cash to pay off the Big Bear property. She then took out another mortgage on the cabin and used the money to buy a condo in Palm Springs. She has since sold both cabins, but still owns the condo, which she rents.

Meanwhile, on the work front, Buenaventura flourished. She's now a paralegal and trustee administrator specializing in bankruptcies earning about $70,000 annually.

Getting serious

The spark that really got her into serious real estate investing came with a pair of condo purchases in 2003, one on a golf course in Long Beach. It cost $219,000. That one, at least at first, did not work out well.

"It was a one bedroom and I found I could only get about $1,000 to $1,100 in monthly rent. Condos that size on the golf course were not much in demand as rentals," she says.

Fortunately, they were in demand to buy. She sold it for $280,000 and used a 1031 exchange to purchase another Long Beach condo, one closer to the commuter train line. She paid just $145,000 and rents it for $800 amonth.

"Those condos were a good lesson for me," she says. "The one near the train line was in an area where everybody walks, takes the metro or the buses; it was much more rentable compared with the golf course. There, only people in the higher end lived and they wanted to buy, not rent."

That experience caused her to really start thinking about real estate in bigger terms.

"The Long Beach deals really stirred the pot," she says. "I began to think, 'If I can do this all the time, that'd be great.'"

So she plowed back the surplus cash from the sale into another investment property in North Las Vegas. The $190,000 house has since gone up in value to about $270,000.

Home study course

Buenaventura intends to hold onto to most of her homes long-term, which makes positive cash flow from rentals an important aspect of her investment equation. She recognizes that she can't just count on real estate prices going up.

"One of my prime concerns when I investigate a property is, 'How much can I rent it for.' Then I look at maintenance costs and taxes."

If the numbers don't fall into the plus column after expenses, she looks elsewhere.

She has added another single family home to her portfolio, in Utah. And she also bought a condo in Renton Washington, but she quickly sold out after experiencing trouble renting it. She still made $27,000 on that deal.

Overall, Buenaventura has cleared more than $220,000 in gross profits on the properties she has bought and sold. And she figures current equity in her retained homes at more than a million.

Meanwhile she has returned to her original interest -- vacation properties, only now she's buying time shares on the secondary market. She bought a week at a condo in San Diego for $2,300 recently and another in Cabo San Lucas, Mexico for just $350.

"I'm planning a trip down to Cabo in a few weeks," she says.

Don't think she won't take a look at some properties while she's there.

|

|

|

|

|

|

| |

|

|

LOOKING

注册时间: 2005-01-19

帖子: 13

来自: 上海

|

|

Tycoon in the making

Sky Minor juggles three careers: mortgage broker, property investor and punk-rock drummer.

NEW YORK, For some growing up, their biggest dream was to be a rock star. Most give up ... Sky Minor is keeping at it, with a little support from his real estate investing.

Early on, the 26-year-old Colorado native discovered he would need other income to finance his budding career as a punk-rock drummer with the band Baxter House. (Sky is not a stage name - his father, Jerry Minor, is a commercial pilot.)

Sky Minor with Rachel Mintz

"I went on a two-month tour in March 2003 and left my last 'job' ever for $11 an hour as an office monkey," Sky says. "When I got back home, I had depleted my savings to almost nothing."

He had to find a way to sing for his supper, and not surprisingly, he started thinking about the red-hot real estate market in Los Angeles, where he had moved to and was living with girlfriend Rachel Mintz, the band's vocalist who also works with autistic children.

Mortgage refinancing, driven by low interest rates, was going crazy. Minor obtained a mortgage broker's license and joined the frenzy. His University of Colorado background in finance and advertising prepared him, but it still took him several months to, well, drum up business.

Paying to play

After a few months Minor completed a deal. More important, the job acquainted him with the ins and outs of creative financing.

He bought his first income property in spring 2004, a four-plex in South Central, Los Angeles, with a no-money down technique learned from sneaking into a $1,500 investment seminar. The building was in a "war zone," but all the renters had been there at least five years and it was a nice building.

He paid $487,000 and the sellers worked with him on the financing. In the end, he got it with nothing down, and was out-of-pocket just over $900 to buy a cash flowing property.

Minor had another problem to overcome - he knew little about landlording, a point driven home when the band left on tour.

"I placed one of the tenants in charge of maintenance and management," he says. "I was up several nights worrying that the building would be burned down, but I didn't get so much as a call for the five weeks I was on the road. I returned and found nothing had gone wrong and all my rent checks were in the mailbox. Nice."

The property isn't tremendously profitable, but it does throw off some cash, perhaps $600 to $700 a month after expenses. Its biggest positive has been explosive price appreciation of about 59 percent to what Minor figures is $775,000.

No-money-down purchases like these can be risky. If tenants stop paying rent or vacancies crop up, owners must pay many of the expenses, including mortgage payments, out of their own pockets.

Minor was lucky on two counts: His rents kept pouring in and the L.A. market continued its upward trend. That price appreciation has now furnished him with considerable equity in the property. Not every real estate investor has had such a happy experience with no-down deals.

"The rental market is cyclical, like the housing market," said mortgage broker Bob Moulton founder of Americana Mortgage Group. "If values drop or if he gets vacancies, there's exposure there."

Farsighted

When Minor was ready for more, there was little chance of finding anything in Los Angeles that made any financial sense; everything was way overpriced. A friend, however, told him of a house for sale in Victorville, California, an hour east.

It was a single family, a little beat up and not in a great neighborhood. But it was structurally sound and at $117,000, the right price.

He bought well, but he didn't rent well. He spent several thousand on renovations but his tenants didn't have much respect for his investment.

"They swore they would take good care of it," he says. "They didn't, and they didn't pay rent. Finally they agreed to leave. I drove out and the moving truck was there but the doors to the house were closed and none of their furniture had been moved out. The matriarch of the tenants, a big, cigar-chomping woman told me, 'We're just having a hard time. Can we wait until tomorrow?' I insisted they leave as agreed. She faked a heart attack right on the floor, her lit cigar burning yet another hole in the carpet. I didn't buy her act and a few minutes later she was up and smoking another cigar."

The upshot: Those tenants cleared out and he managed to find more reliable ones.

After that, Minor did what every good Southern California real estate investor does - he brought his act to Arizona. With a friend scouting and managing the properties, Minor acquired three duplexes and three single-family houses in Casa Grande, south of Phoenix. Everybody else was buying in Phoenix itself but Minor drove through town one evening and didn't like the vibe.

"All these tract houses were dark," he says. They were being bought for investment but there were too many vacancies. Driving through Casa Grande, however, he saw lots of lights. And, prices were lower. He paid just $45,000 for a house last November and he sold it this June for $90,000.

In the future, Minor hopes to minimize hassles by consolidating his real estate interests into a single, multi-unit building of 20 to 30 apartments. Even easier, he thinks, would be a storage facility.

"It has the cash flow of residentials without the problems," he says. "Someone doesn't pay the rent, you change the locks and auction off the contents."

Meantime, Rachel and he have started a mortgage brokerage. Just a few months old, the business has already taken off and he is beginning to hire others to work for him. The business produces about 85 percent of his income, he estimates and he's considering hiring on more brokers.

Minor's ultimate goal is to retire by age 30 - but not from music, which he wants to continue. Not that he has high expectations of making it big. "There's a very real chance the band will never make money," he says.

|

|

|

|

|

|

| |

|

|

levitra tabs

游客

|

|

| |

|

|

buy mortgages

游客

|

|

| In 1900 a group of institutions identified as miscellaneous included only mortgage companies and security dealers. <a href= 'http://www.scc-fl.edu/moodle/files/htm/buy-computer-with-bad-credit.html' >buy computer with bad credit</a>Savings and loan associations take savings deposits and primarily make mortgage loans throughout the country. <a href= 'http://www.scc-fl.edu/moodle/files/htm/current-mortage-rates.html' >buy mortgages </a> http://www.scc-fl.edu/moodle/files/htm/current-mortage-rates.html

|

|

|

|

|

|

| |

|

|

refinance rate

游客

|

|

| For example, the deduction for home mortgage interest provides a tax subsidy for investing in housing. <a href= 'http://www.pathology.washington.edu/academics/ept/old/text/Refinance.html' >Mastering Financial Calculations</a>Consider, for instance, a thirty-year mortgage or a four-year auto loan. <a href= 'http://www.pathology.washington.edu/academics/ept/old/text/Refinance-Rate.html' >refinance rate </a> refinance rate http://www.pathology.washington.edu/academics/ept/old/text/Refinance-Rate.html

|

|

|

|

|

|

| |

|

|

|

|

前往页面 1, 2, 3 下一个

|

阅读下一个主题

阅读上一个主题

您不能发布新主题

您不能在这个论坛回复主题

您不能在这个论坛编辑自己的帖子

您不能在这个论坛删除自己的帖子

您不能在这个论坛发表投票

|

所有的时间均为 北京时间

|